In plain English

A retail trader sees a Polymarket contract priced at 67 cents. The headline event seems likely. The trader buys YES at 67. Three weeks later, the event happens, the contract resolves at $1.00, and the trader pockets 33 cents per share. Skill?

It depends on a number the trader almost certainly did not write down: their own probability of YES at the moment they bought. If they would have priced it at 67% themselves, the trade was a coin-flip with no edge that happened to land. If they would have priced it at 80%, there was a 13-cent edge per share and the trade was correctly identified. If they would have priced it at 60%, the trade was a negative-edge bet that got bailed out. Same outcome, three completely different stories. This entry is about the missing number.

Why agreeing with the market price is not edge

Edge in a directional trade is the gap between the trader’s probability and the market’s price. When the two match, the expected value of the trade is zero before fees and negative after fees. Whether it wins or loses is luck.

Retail PM traders often confuse the feeling of confidence with edge. A market priced at 67 that ‘feels right’ is, by definition, a market the trader agrees with. Agreement produces no edge. The only way to make consistent expected value on a directional book is to systematically hold probabilities that differ from the market’s, and to act on those differences.

The cost of mirroring the market is not just zero edge. It is also inheriting the market’s mistakes. Polymarket and Kalshi prices exhibit a favourite-longshot bias (Whelan 2026 on Kalshi data, with similar patterns documented across other PM venues): low-priced contracts win less often than their prices imply, high-priced contracts win slightly more often. A trader who does no independent work and trades the venue prices is shipping that bias into their book.

The two numbers edge needs

P_market is the price the venue is showing. It is not, technically, a probability; it is a price. On a deep market with active arbitrage, it approximates the consensus probability of the event closely. On a thin or stale market, the gap between price and consensus probability can be meaningful (taker fees, slippage, and fee-aware net gap discipline are the topic of the cross-venue arbitrage entry). For directional purposes, treat P_market as the price the trade will execute at and reason about edge from there.

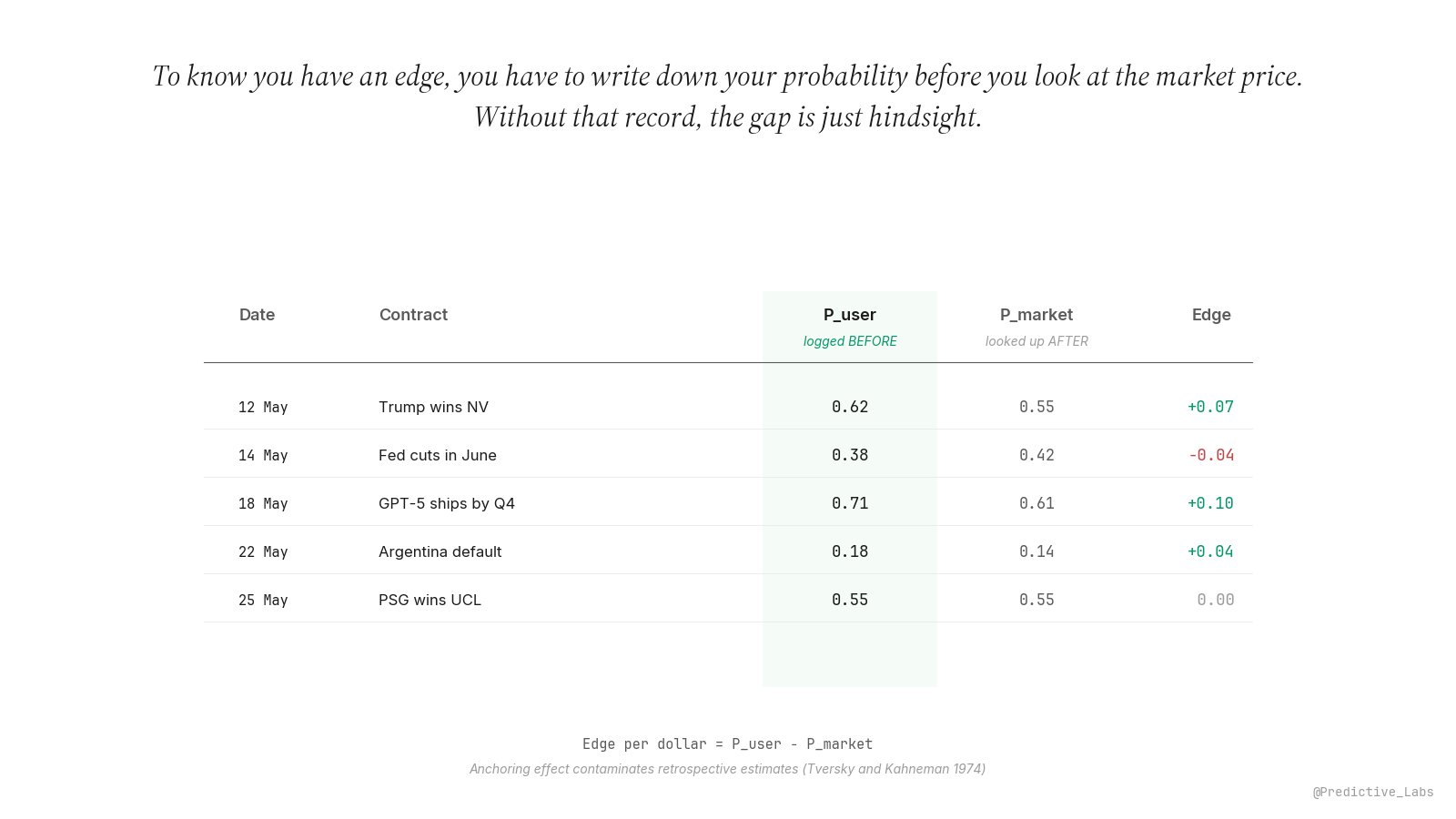

P_user is the trader’s own probability of the YES outcome resolving. It has to come from somewhere outside the venue: base rates on similar past events, primary research, structural reasoning, a forecasting model, an aggregation of independent sources. The specific method varies. The discipline is that P_user is a number formed before looking at P_market and written down before the trade is placed.

Edge is then a single subtraction:

Edge = P_user − P_market

Positive edge on a YES trade is a buy candidate. Negative edge is a sell candidate (or a buy on NO at 1 minus P_market). Zero edge is no trade. The edge size, in cents, is what feeds the Quarter Kelly sizing rule: bigger edge means bigger size, but never more aggressively than a quarter of the full Kelly fraction.

How to log P_user without contaminating it

The biggest practical problem with P_user is that human probability estimates anchor on whatever number was seen first. Tversky and Kahneman (1974, in Science) document the anchoring-and-adjustment heuristic: when people are asked to estimate a quantity after exposure to an arbitrary reference value, their estimates pull strongly toward that reference, even when the reference is irrelevant or random. Anchoring is robust, replicated extensively, and stronger than most people believe of themselves.

In a PM context, the reference is the market price. A trader who looks at a 67-cent contract and then asks themselves ‘what do I think the probability really is?’ will produce a number that has 67 baked into it. If they would have said 80% from primary sources, they may write down 73%. If they would have said 50%, they may write down 60%. The logged P_user is partly a derivative of the anchor, which means the logged edge is understated when the trader genuinely disagrees with the market and overstated when the trader is unconsciously matching it.

Three working rules to break the anchor:

1. Form P_user from primary sources first. Base rates, structural arguments, model output, independent research. Assemble the number without opening the market.

2. Write it down before checking the price. A pre-trade log entry with timestamp, contract, and P_user, locked before P_market is seen. This is the entire discipline. Skipping it converts the entry to a post-trade rationalisation, which is statistically worthless.

3. Only then check P_market and compute edge. If the gap is meaningful (and survives fees and slippage), the trade is on. If not, log the candidate as a no-trade and move on.

What 100 logged probabilities actually buy you

One pre-trade probability tells the trader nothing. Ten tell them very little. At around 100 logged probabilities, the dataset becomes statistically useful for three concrete tools.

Brier score with usable confidence intervals. A Brier score on 30 trades has wide uncertainty bands; the difference between a 0.10 and a 0.14 score in that sample is not statistically significant. At 100 trades, the score starts to discriminate. The Brier Score companion entry covers the benchmark levels.

Calibration curve with non-noise bins. A 10-bin calibration curve needs roughly 10 trades per bin to give stable readings. With 100 trades evenly spread across the range, every bin is in the informative zone. The calibration curve entry covers the diagnostic shapes.

Kelly-correct sizing. The Kelly fraction depends on edge size, and edge depends on P_user. With 100 honest probabilities, the trader has enough data to estimate their own typical edge magnitude and to apply the Quarter Kelly rule with confidence. The Quarter Kelly entry covers the sizing rule itself.

Below 100, none of the three tools are stable enough to act on. Above 100, the trader is operating with a performance dataset rather than a hunch. The threshold is not magical, but it is roughly where the literature on probabilistic forecasting evaluation puts the lower bound of useful inference.

How this lives in nijinn

The Informed Directional Surface in nijinn enforces P_user logging before the trade. The trader enters their probability, the surface holds it, and only then is the market price displayed and the edge computed. The pre-commit pattern is built into the workflow. The logged probability flows into Brier, calibration, and Kelly sizing automatically, so the discipline that breaks the anchor is the same discipline that produces the performance dataset.

The metric pairs naturally with calibration curve on the audit side and with Quarter Kelly on the sizing side. A trader who logs P_user honestly, sizes by Kelly, and audits by Brier and calibration is operating with the three-leg stool that retail PM trading almost never has. Without P_user, none of the legs work.

Edge is the gap between two numbers. Most traders only have the market’s. Logging the other one, before the anchor lands, is the trade.