In plain English

A trader sees a YES contract on Polymarket priced at 50 cents and thinks the real probability is closer to 60. Edge identified. Now the harder question: how much of the bankroll goes into this trade? 100 dollars? 500? 5,000?

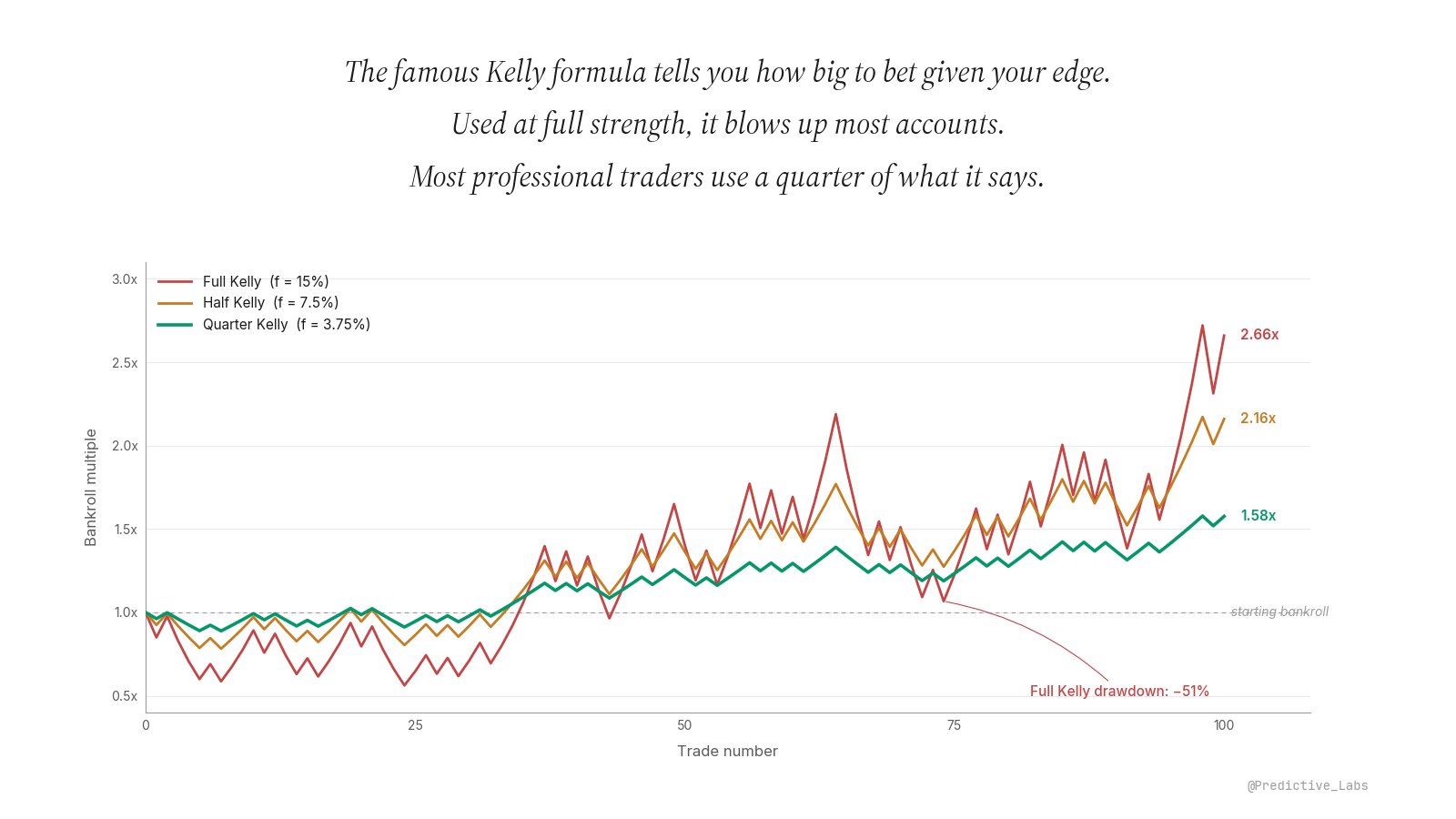

The Kelly criterion is the formal answer to that question. Published by John L. Kelly Jr. at Bell Labs in 1956 (Bell System Technical Journal, Vol. 35, pp. 917-926), it gives the bet size that maximises the long-run growth rate of the bankroll. Used at full strength, it is also the bet size that flattens most retail accounts. The professional move is to compute Kelly, then bet a quarter of it.

Why gut and fixed-percent both fail

Most traders size their positions one of two ways. They size by gut (this one feels right, send it) or they apply a flat percentage of bankroll to every trade (always 2%, always 5%). Both look disciplined from the outside. Both are wrong, in opposite directions.

Gut sizing overweights conviction and underweights calibration. The trade that feels strongest is often the trade where the consensus is already correct, because conviction is built from the same news flow the market already priced in. Gut also ignores the actual edge: a trader who feels equally strongly about a 1-cent edge and a 10-cent edge sizes them similarly, leaving 9-to-1 capital efficiency on the table.

Fixed-percent sizing has the opposite failure. It treats every opportunity the same. A 0.5% edge on a 50-cent contract gets the same capital as a 15% edge on the same contract. That is not risk discipline. That is risk indifference. The whole point of having an edge is to deploy capital in proportion to it.

Kelly fixes both problems by tying size directly to the size of the edge.

How Kelly’s formula actually works

The general Kelly fraction is your edge divided by the odds you face. For a binary prediction-market contract priced at c dollars with your private probability of YES equal to p, the formula simplifies cleanly:

f* = (p − c) / (1 − c)

The numerator is your edge in price terms (your probability minus the consensus price). The denominator is the maximum profit per dollar bet on YES (a contract you bought at c can rise to a maximum payout of 1 dollar). Multiply the result by your bankroll and you have the dollar size of the position under full Kelly.

Worked example · Full Kelly on a 50-cent contract

Quarter Kelly is Full Kelly multiplied by 0.25. A 15-cent edge on a 50-cent contract has Full Kelly recommending 30% of bankroll on a single trade. The Quarter Kelly version is 7.5%, which most traders can survive a losing run on. The Full Kelly version, most cannot.

Bigger edges command bigger sizes, and the formula is linear in the edge. That linearity is what makes the Full Kelly numbers escalate so quickly: a 15-cent edge is three times the size of a 5-cent edge, but the recommended bet is also three times bigger, on the same contract, with the same downside.

Why Full Kelly devastates real accounts

Three problems break Full Kelly in the real world.

The first is parameter uncertainty. The formula assumes you know p exactly. You do not. Real probability estimates carry measurement error: maybe your true edge is 5 cents, maybe it is 2, maybe it is zero and you are fooling yourself. The Kelly fraction is highly sensitive to that error. A trader who overestimates their edge by 10% will see the formula recommend roughly twice the position size that actually maximises growth. Overestimate by 25% and the formula prescribes a wildly overlevered bet on a contract you barely have an edge on.

The second is path. Kelly maximises expected log-wealth over many trades, which is the right objective in the limit. The path to that limit runs through punishing drawdowns. Full Kelly produces peak-to-trough drawdowns of roughly 50% during typical extended sequences, even with a real edge and accurate probabilities. A trader losing half the bankroll en route to the long-run optimum is mathematically on track. Almost no human is psychologically on track. The strategy gets abandoned at the deepest drawdown, which is exactly when it would have started recovering.

The third is friction. The Kelly model assumes continuous, instant, frictionless betting. Polymarket and Kalshi have taker fees, slippage on size, limit orders that do not always fill, and resolution risk that the formula does not account for. Each friction effectively reduces the realised edge below the modelled edge, which means Full Kelly is overbetting against reality.

Why exactly Quarter Kelly, and not Half or one-third

Fractional Kelly is the standard professional response to all three problems above. The literature, summarised most clearly in Thorp (2008) and MacLean, Sanegre, Zhao and Ziemba (2004), gives the math:

Half Kelly captures roughly 75% of the long-run growth rate at roughly half the variance. Quarter Kelly captures roughly 50% of the growth rate at much lower variance again. The growth-versus-survivability trade-off becomes flat once you go below a quarter, so smaller fractions cost more growth than they save in drawdown.

The multiplier applied to Full Kelly. Lower is more conservative. The survival zone is the left.

The choice between a quarter and a half comes down to how confident you are in your probability estimates. A trader with a long, audited record of well-calibrated forecasts on a specific category can run Half Kelly without much risk of blowing up. A trader without that record, working with a noisy probability estimate, on a fat-tailed binary contract that may not fill at the price they want, should run Quarter Kelly. Ed Thorp, who pioneered Kelly applications in finance, used Half Kelly. Many top quantitative funds run something closer to Quarter Kelly because the cost of blowing up vastly exceeds the value of slightly faster growth.

For prediction-market traders specifically, all three of those conditions apply: probability estimates are noisy (you are not running a Renaissance-grade model), payoffs are binary and fat-tailed (a wrong call costs the full position), and limit orders may not fill at the price the formula assumed. Quarter Kelly is the right starting point. Move toward Half only after the calibration record justifies it.

How this lives in nijinn

Quarter Kelly is the default sizing on the Informed Directional Surface. nijinn pulls the contract price from Polymarket or Kalshi, takes the probability you logged before opening the trade, computes the full Kelly fraction, multiplies by 0.25, and surfaces the dollar size and percentage-of-bankroll size as the recommended position. The 0.25 multiplier is overridable per trade for traders with the calibration record to justify Half Kelly, but the default is fixed at a quarter for new accounts.

The discipline pairs naturally with P_user versus market price, which is where the probability estimate gets locked in before the trade, and with Brier Score, which is the audit on how well-calibrated your probability estimates have actually been. Kelly without a calibration audit is sizing in the dark. Calibration without sizing is forecasting without execution. The two metrics work together.

Kelly is fast money. Quarter Kelly is staying-in-the-game money. Most traders choose the second only after losing badly with the first.