In plain English

A market maker quotes both sides of a Polymarket contract for a four-hour session. Plenty of fills land on each side. At the close, the dashboard shows +$1,000. Good day?

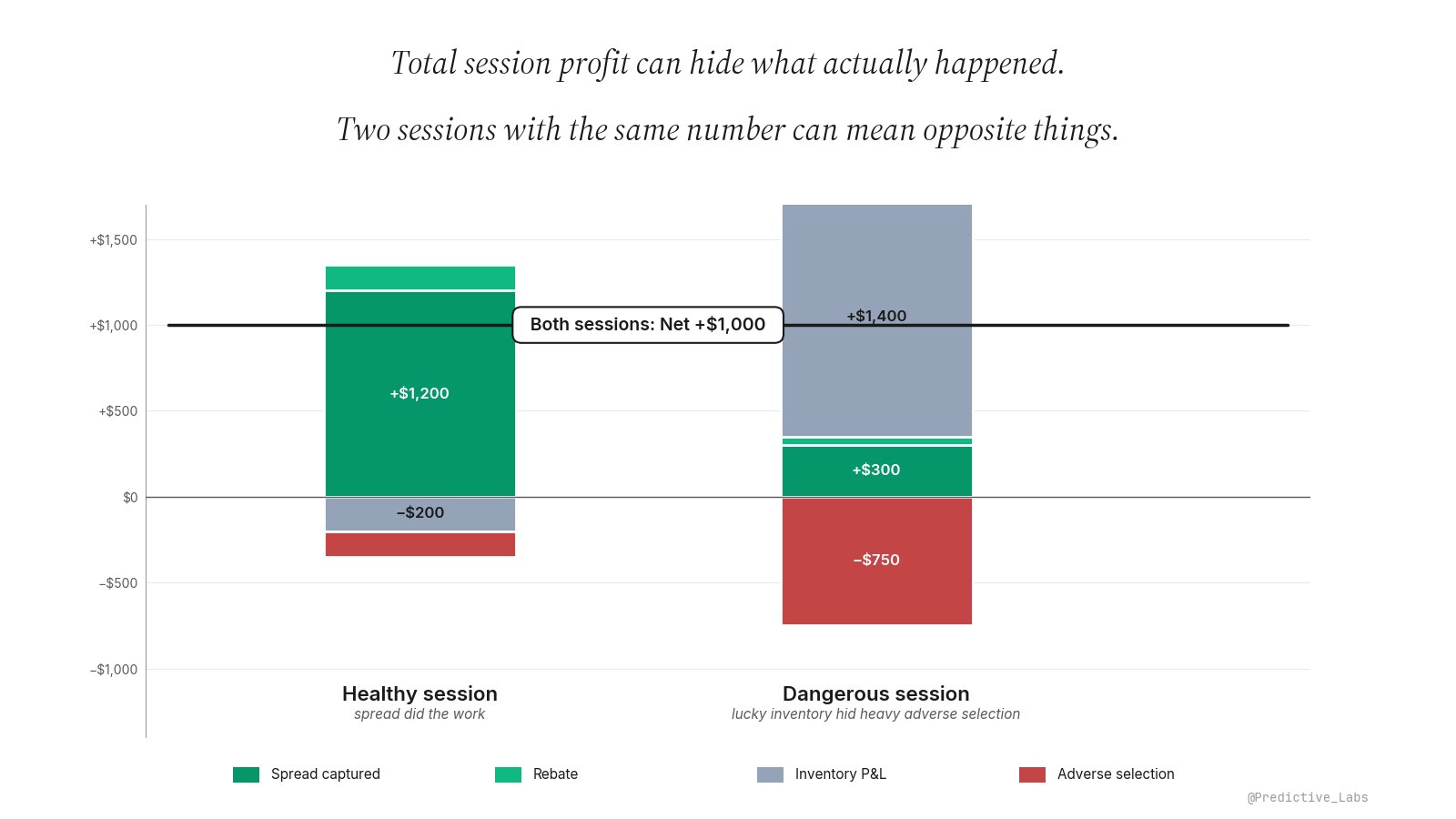

That depends entirely on which of 4 things drove the number. The same +$1,000 can come from a tightly run quoting book where the spread did the work, or from an exposed book that got bailed out by a lucky inventory move while paying a brutal adverse-selection cost. Same total, opposite operations, opposite to-do lists. This entry is about the decomposition that tells the two apart.

Why total P&L hides what actually happened

Market-making P&L is the sum of four largely independent income streams. Each one is a real thing the desk earns or loses on, and each one carries different information about what the market maker actually did.

The trouble is that the four streams cancel and offset constantly. A good day on adverse selection (no informed flow) can mask a session where the maker barely captured any spread. A bad day on inventory (a position that drifted against the desk) can drown out a perfectly executed quoting performance. Total P&L tells the desk only that the four numbers added up to a positive sign on this particular afternoon. It tells the desk nothing about whether to keep doing what it did.

The classical literature on market-maker spread decomposition (Glosten and Harris 1988, Huang and Stoll 1997) makes the same point in different language: the spread the maker quotes has to compensate for order processing, inventory holding, and adverse selection, and the maker’s realised P&L is the residual after each of those costs is paid. The four components below are the realised version of that accounting.

The 4 components, plainly

1. Spread captured. Every time both sides of the maker’s quote get filled, the desk earns the difference between the bid and the ask. On a 1-cent quoted spread with 1,000 round-trip fills in a session, spread captured is approximately $10. This is the income stream the operation is built on. It is the only component the maker has direct control over, through how wide and how aggressively they quote.

2. Maker rebate. Some venues pay makers a credit for providing liquidity, funded by taker fees. Polymarket international redistributes roughly 25% of taker fees to makers daily (20% on Crypto), and the Polymarket US exchange offers a 0.20% maker rebate on contract premium. Kalshi did not charge makers before April 2025 but introduced a maker fee at roughly a quarter of the taker rate after that date, so makers there now pay rather than receive. The rebate (or fee) is small per fill but accumulates linearly with volume.

3. Inventory P&L. When fills are unbalanced, the maker carries inventory that did not close out within the session. That inventory marks to market against the latest reference price. If the maker is long 500 contracts at an average of 52 cents and the contract closes the session at 55, inventory P&L is +$15. If it closes at 49, inventory P&L is -$15. This component is mostly noise. A session with positive inventory P&L is not a session where quoting was good. It is a session where the residual position happened to drift the right way.

4. Adverse selection. When the maker’s fills systematically trade against them in the seconds and minutes after the print (the market moves up after a maker sold, down after a maker bought), the difference is adverse selection. It is the cost of trading with counterparties who know more than the quote did. Measured cleanly via post-fill price drift over a 1-minute or 5-minute window, it is the only component that should keep a market maker up at night, because it compounds silently inside total P&L until the spread the maker is capturing no longer covers it.

Two sessions, same total, opposite stories

The two sessions print the same number on the dashboard. The healthy one was earned through quoting; the dangerous one was rescued by an inventory swing while paying $750 in adverse selection. The right response to each is opposite.

What to fix when each component dominates

Spread plus rebate dominant. The desk is being paid for what it is doing. Quoting is working, the venue is rewarding liquidity, and the size being run is appropriate to the book. Nothing to fix. Scale up only if the depth and toxicity profile of the contract supports it.

Inventory P&L dominant (positive or negative). The maker carried an unbalanced book and the contract drifted. The same setup with the opposite drift would have produced an equal and opposite number, with no change in skill or method. Treat it as zero information about quoting quality. The fix on either sign is tighter inventory management: more aggressive rebalancing, smaller maximum position limits, and a hard cap on time spent away from a balanced book. The temptation after a negative result is to widen the spread to compensate, but the spread was not the problem. The position-management discipline was.

Adverse selection dominant negative. This is the dangerous one. Counterparties are systematically better informed than the maker’s quotes. Three textbook responses, in order of escalation: widen the spread on the contracts where post-fill drift is highest, pull quotes around scheduled events (FOMC meetings, debates, jobs reports, league announcements) where informational asymmetry spikes, and reduce size on contracts whose order flow shows rising toxicity (often measurable through VPIN or simpler post-fill drift summaries). Sustained adverse selection that the spread cannot absorb is a signal to stop quoting that contract entirely.

How this lives in nijinn

The Market Making Surface in nijinn breaks every session into the 4 components live. Spread captured comes from the quote-and-fill log, rebate is computed from the venue-correct fee schedule, inventory P&L marks open positions to the rolling reference price, and adverse selection is calculated from post-fill drift over a configurable window. The session view shows the four bars side by side, the way the diagram above shows two sessions side by side, so the maker can read the story behind the headline number rather than the number alone.

The metric pairs naturally with the adverse-selection deep dive (the standalone counterparty-informedness metric, derivable from VPIN and post-fill drift) and with the 4-method fair-value comparison that drives the quoting itself. P&L attribution is the audit; fair value and quoting are the inputs.

A +$1,000 day is not a +$1,000 day until the maker knows which of the 4 components paid for it. The same total can be a result or a warning.